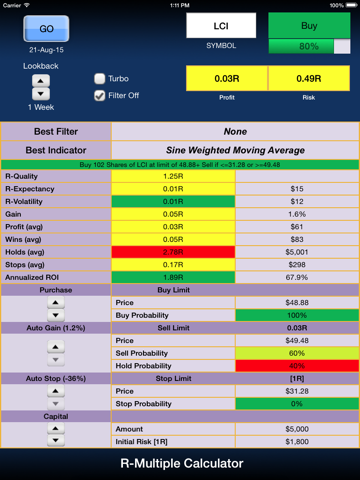

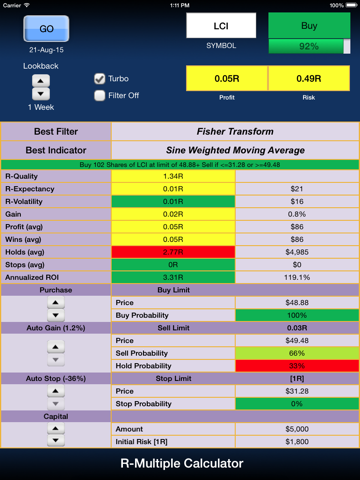

Every Trading System can be described by the R-multiples, irregardless of the trade size or stock values.

R-multiple brings uniformity to analyzing stock performance and position sizing where all data is a multiple of the Initial Risk. For example, with 1R initial risk of $50 with a 2R profit equals $100. A Loss equal to -$25 equals -0.5R. The R-Multiples are automatically (or manually) backtested using multiple filters and technical indicators. Using historical data, stocks are purchased every day during the back-test period as defined by filtering rules and immediately sold as defined technical indicator criteria. The four built-in filters are, Zero-Lag MACD, ADX, RVI, Fisher and Turbo (proprietary algorithm).

The R-multiple Calculator determines R-multiple performance for:

- Profit

- Trade Quality

- Expectancy

- Volatility

- Initial Risk

- Gain

- Wins, Holds and Stops

- Annualized ROI

- Position Sizing