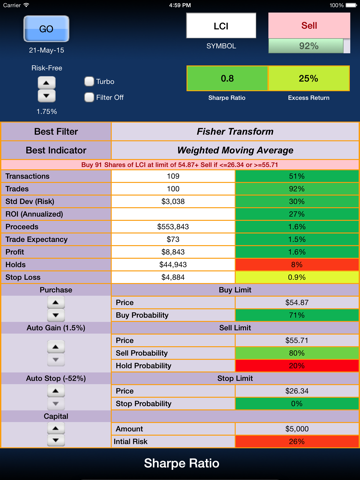

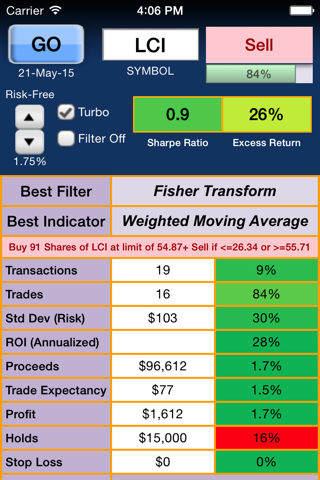

Increase profitability by achieving the largest return per unit of risk.

The Sharpe Ratio has become one the most widely used investment ratios for measuring risk or return. Composed of only three components, the formula establishes a relationship with any Risk-Free investment for comparing the returns. Higher ratio's result in a higher excess return and greater profitability.

The Sharpe Ratio and Excess Return is automatically calculated over a 6-month period using historical data with the following modes:

1. All - Buy-Sell the security each day for 6-months with no regard to the quality of the transaction.

2. Technical Indicators - Automatically finds the best gain for each transaction.

3. Fixed Gain - The gain is the same for each transaction.

4. Technical Filters - Uses selective filter criterion to filter potentially risky buys.

5. Turbo - An aggressive risk based filter to eliminate remaining holds and stops.

A trading statement is produced for each Buy-Sell Signal specifying the number of shares, purchase price limit, sell price limit and stop price limit.

Additional data for the 6-month period is:

1. Number of Transactions

2. Number of completed

3. The Standard Deviation associated with the Sharpe Ratio

4. Annualized

5. Gross Proceeds

6. Trade Expectancy

7. Gross Profit

8. Gross Holds

9. Gross Stops